When navigating the world of real estate, homeowners often come across unfamiliar terms—one of the most common being “paid in arrears.” But what does it really mean, and how does it impact you as a homeowner? In simple terms, “paid in arrears” refers to payments made after a service, period, or obligation has already been fulfilled. Whether it’s property taxes, mortgage payments, or utility bills, understanding this concept is crucial for managing your finances effectively and avoiding confusion during real estate transactions.

What Does “Paid in Arrears” Mean?

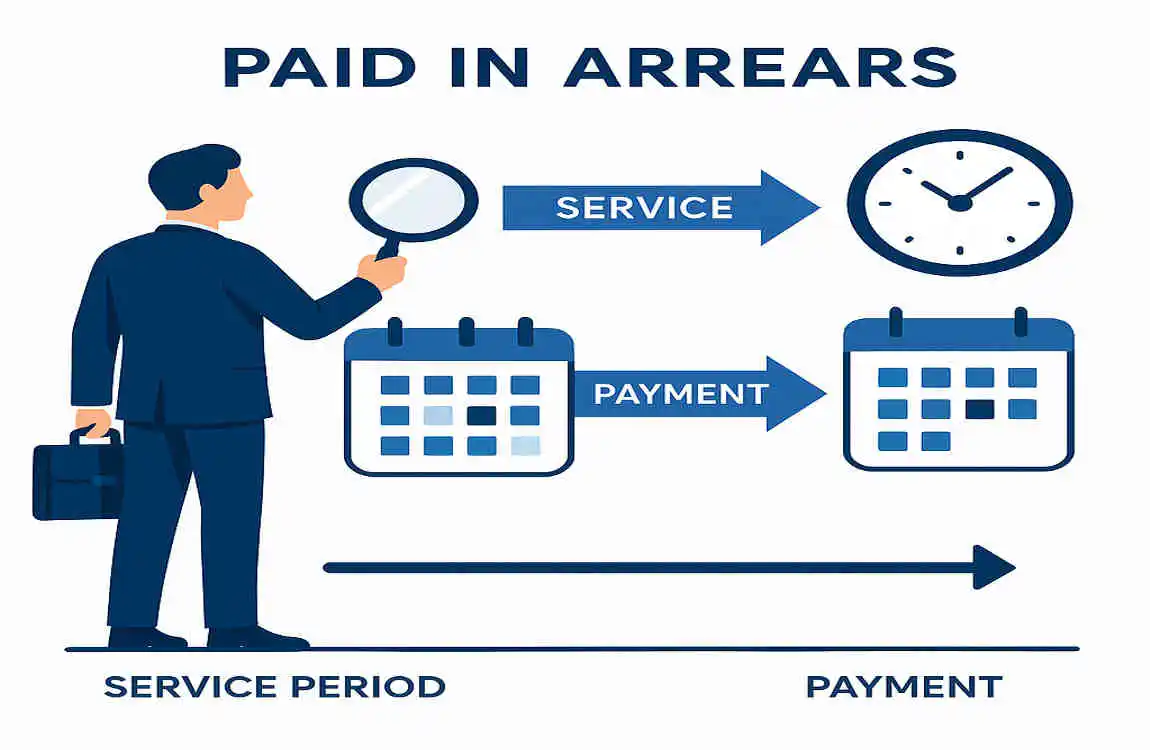

Definition of “Paid in Arrears”

Let’s start with the basics. When a payment is made “in arrears,” it means that the payment is made after the service or period it covers has already been completed. In other words, you’re paying for something that has already happened, rather than paying upfront.

For example, imagine you’re renting a home. If your rent is due on the first of the month, but it’s for the previous month’s stay, that’s a payment in arrears. You’re essentially paying for the time you’ve already spent in the rental.

Difference Between “Paid in Arrears” and “Paid in Advance”

Now, let’s compare “paid in arrears” to its counterpart, “paid in advance.” As you might guess, “paid in advance” means you’re paying for a service or period before it happens.

To illustrate the difference, let’s look at two real estate scenarios:

- Paid in Arrears: You close on your new home on June 15th. Your first mortgage payment is due on August 1st, but it covers the interest for July. You’re paying for the previous month’s interest in arrears.

- Paid in Advance: You purchase a homeowner’s insurance policy that covers you from January 1st to December 31st. You pay the full premium on January 1st, before the coverage period begins. This is an example of paying in advance.

Here’s a handy table to help you remember the key differences:

| Payment Type | Definition | Real Estate Example |

|---|---|---|

| Paid in Arrears | Paying after the service or period has been completed | Mortgage payment due on August 1st for July’s interest |

| Paid in Advance | Paying before the service or period begins | Homeowner’s insurance premium paid on January 1st for the entire year |

How “Paid in Arrears” Applies to Real Estate Transactions

Property Taxes

One of the most common areas where “paid in arrears” comes into play in real estate is property taxes. In many jurisdictions, property taxes are billed and paid in arrears.

Mortgage Payments

Another key area where “paid in arrears” is relevant is mortgage payments. When you take out a mortgage, your monthly payments typically include both principal and interest. However, the interest portion of your payment is usually calculated and paid in arrears.

Utility Bills

Lastly, utility bills in real estate are often billed in arrears. When you receive your monthly utility bill, it typically covers the usage from the previous month. So, if you get your bill on September 15th, it’s likely for the electricity, water, or gas you used in August.

Why Homeowners Need to Understand “Paid in Arrears”

Financial Planning

Understanding how “paid in arrears” works can be a game-changer when it comes to financial planning as a homeowner. By knowing when certain payments are due and what they cover, you can better budget for your housing expenses.

For example, if you know that your house property tax bill is due in arrears, you can set aside money throughout the year to cover that expense. Similarly, understanding that your mortgage payments include interest from the previous month can help you plan your cash flow more effectively.

Avoiding Confusion During Transactions

Real estate transactions can be complex, and the way payments are structured can sometimes lead to confusion. By having a clear understanding of “paid in arrears,” you can avoid misunderstandings and ensure that all parties involved are on the same page.

When you’re buying or selling a home, there may be prorated payments for things like property taxes or utility bills. Knowing how these payments are calculated and who is responsible for them can help you navigate the closing process smoothly.

Legal and Contractual Implications

“Paid in arrears” can also have legal and contractual implications in real estate. When you enter into a sales contract or mortgage agreement, the payment terms are typically spelled out in detail.

How “Paid in Arrears” Impacts Homebuyers and Sellers

For Homebuyers

As a real estate homebuyer, understanding “paid in arrears” can help you navigate the closing process and plan for your ongoing expenses.

When you’re buying a home, you may be responsible for prorated payments for things like property taxes or utility bills. These payments are typically calculated based on the number of days you’ll own the property during the billing period.

Common Misconceptions About “Paid in Arrears” in Real Estate

“Arrears means you’re late on payments.”

One common misconception about “house paid in arrears” is that it means you’re late on your payments. However, this is not the case.

When a payment is made in arrears, it simply means that you’re paying for a service or period that has already been completed. It doesn’t imply that you’re behind on your payments or that you’re in default.

“All real estate payments are in arrears.”

Another misconception is that all real estate payments are made in arrears. While this is true for many types of payments, such as property taxes and mortgage interest, there are exceptions.

“Arrears only affect property taxes.”

Finally, some people believe that “paid in arrears” only applies to property taxes. However, this concept can apply to various aspects of real estate, including:

- Mortgage payments (interest portion)

- Utility bills

- Rent payments (in the case of rental properties)

Understanding how “paid in arrears” applies to these different areas can help you manage your finances and plan for your housing expenses more effectively.

Real-Life Examples of “Paid in Arrears” in Real Estate

Property Tax Payments

Let’s walk through a detailed example of how property tax payments work in arrears during a typical real estate transaction.

Imagine you’re selling your home on June 15th. The house property taxes for the entire year are due on December 31st, but they cover the period from January 1st to December 31st. To calculate the prorated amount you owe, you would divide the total annual tax bill by 365 days and then multiply that daily rate by the number of days you owned the property (January 1st to June 14th).

For example, if the total annual tax bill is $6,000, the daily rate would be $16.44 ($6,000 ÷ 365 days). You would then multiply that daily rate by the 165 days you owned the property ($16.44 × 165 days = $2,712.60). This would be the amount you’re responsible for paying at closing, and the buyer would take over the remaining $3,287.40 in taxes for the year.

Mortgage Payments

Now, let’s look at how the arrears system impacts monthly mortgage payments for homeowners.

When you take out a mortgage, your monthly payment typically includes both principal and interest. However, the interest portion of your payment is calculated based on the previous month’s outstanding real estate balance.

For instance, let’s say your mortgage payment is due on September 1st. That payment would include the interest that accrued on your loan during the month of August. If your outstanding balance at the beginning of August was $200,000 and your interest rate is 4%, the interest for August would be $666.67 ($200,000 × 0.04 ÷ 12 months). This amount would be included in your September 1st payment, along with a portion of the principal.

Closing Transactions

Finally, let’s explore how arrears payments are accounted for in closing costs during a real estate transaction.

When you buy or sell a home, the closing costs can include prorated payments for things like property taxes, utility bills, or HOA fees. These payments are typically calculated based on the number of days the seller owned the property during the billing period.

For example, if you’re buying a home on June 15th and the property taxes are due on December 31st, the seller would be responsible for paying the taxes for January 1st to June 14th. This amount would be deducted from the seller’s proceeds at closing, and you would take over the responsibility for the remaining portion of the year.

How to Calculate “Paid in Arrears” Amounts

Step-by-Step Guide to Calculations

Calculating “paid in arrears” amounts can seem daunting, but it’s actually quite straightforward. Here’s a simple step-by-step guide to help you through the process:

- Determine the total amount due: Start by finding out the total amount of the bill or payment that needs to be prorated. This could be an annual property tax bill, a monthly utility bill, or any other payment that’s made in arrears.

- Calculate the daily rate: Divide the total amount due by the number of days in the billing period. For example, if you’re prorating an annual property tax bill, you would divide the total amount by 365 days.

- Determine the number of days: Figure out how many days the seller owned the property during the billing period. This is usually from the beginning of the billing period up to (but not including) the closing date.

- Multiply the daily rate by the number of days: Take the daily rate you calculated in step 2 and multiply it by the number of days the seller owned the property (from step 3). This will give you the prorated amount the seller is responsible for paying.

- Subtract the prorated amount from the total: Subtract the prorated amount (from step 4) from the total amount due (from step 1). The remaining amount is what the buyer will be responsible for paying.

Tools and Resources for Homeowners

If you’re feeling overwhelmed by the calculations, don’t worry – there are plenty of tools and resources available to help you navigate “paid in arrears” in real estate.

- Online calculators: There are many online calculators specifically designed for prorating payments in real estate. These calculators can help you quickly and accurately determine the amounts due from both the buyer and seller.

- Real estate apps: Some real estate apps, such as those used by real estate agents or title companies, may have built-in tools for calculating prorated payments. Check with your real estate professional to see if they have any resources available.

- Working with a real estate agent: Your real estate agent can be an invaluable resource when it comes to understanding and calculating “paid in arrears” amounts. They have experience with these types of calculations and can guide you through the process, ensuring that everything is done correctly.