Deciding where to put your hard-earned money is one of the biggest milestones you will ever face. You’ve spent years saving, skipping those extra vacations, and keeping a close eye on your bank account. Now, you stand at a crossroads. You are likely asking yourself: “Should I buy an investment property or my first home?”

This isn’t just a financial question; it’s a lifestyle one. Imagine you’re a young professional living in a bustling city like Lahore. You see the skyline changing every day with new high-rises in Gulberg and sprawling phases in DHA. You want a piece of that pie, but do you want a place to hang your hat, or a place that puts money back into your pocket every month.

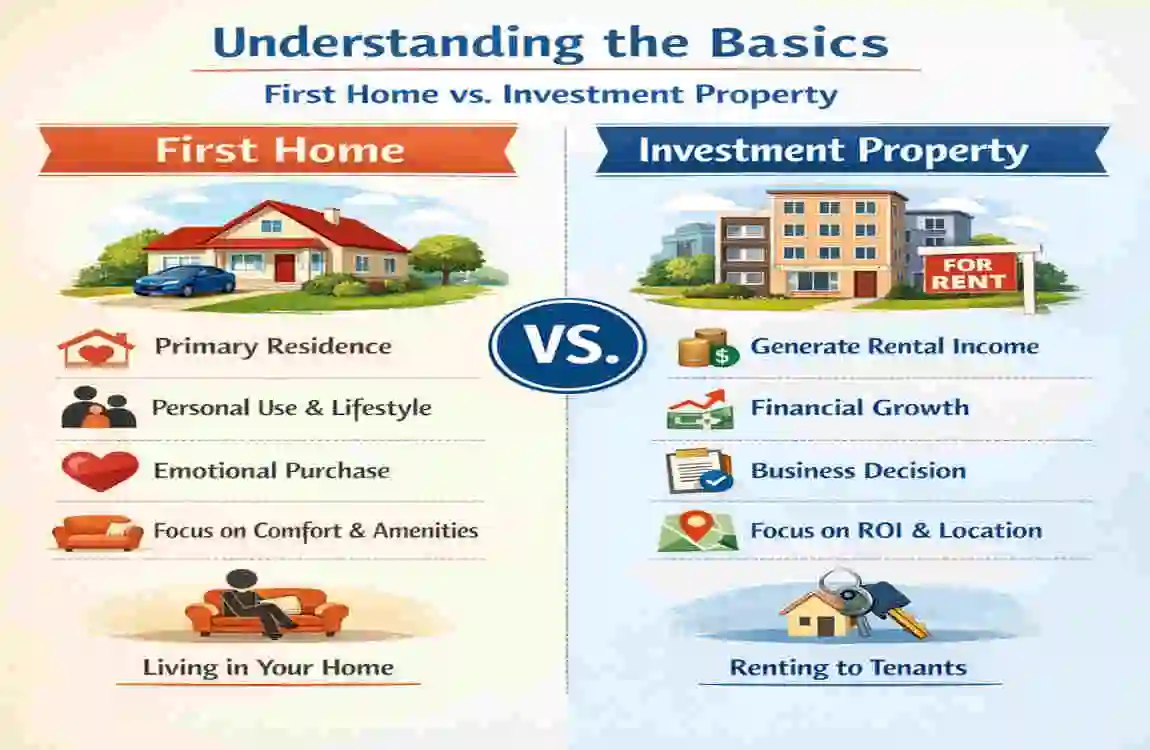

Understanding Your Goals: Investment Property vs First Home

Before you look at a single listing or talk to a real estate agent, you need to look in the mirror. What do you actually want from this purchase? The choice between an investment property and a first home often comes down to a battle between your heart and your wallet.

The Emotional security of a First Home

For many, a first home is more than just bricks and mortar. It is a sanctuary. It represents stability and the freedom to paint the walls whatever colour you like without asking a landlord for permission. In the Pakistani context, owning a home is often seen as a “rite of passage.”

When you buy a first home, your primary return isn’t necessarily cash; it’s utility. You get to live there. You don’t have to worry about sudden rent hikes or being asked to vacate on short notice. Furthermore, the government often provides subsidies or lower tax brackets for first-time buyers to encourage homeownership. If your goal is to build a family and have a permanent base, the first home is usually the clear winner.

The Financial Engine of an Investment Property

On the flip side, an investment property is a business decision. You aren’t looking for a nice kitchen because you want to cook in it; you’re looking for a kitchen that will attract a high-paying tenant.

In cities like Lahore or Islamabad, rental yields can range between 5% and 7%, depending on the locality. An investment property is meant to generate passive income and long-term capital growth. You might choose to live in a small, affordable rented apartment while owning a high-value commercial shop or a residential unit in a prime area. This strategy, often called “rentvesting,” is becoming increasingly popular among savvy investors in 2026.

Which One Fits Your Life Stage?

Are you single and mobile, or do you have a growing family? If you are young and your career takes you to different cities, buying a first home might tie you down. An investment property, however, keeps your capital working while you remain flexible.

FeatureFirst Home (Primary Residence)Investment Property

Primary Goal : Shelter and Emotional security , Wealth Creation and Cash Flow

Main Benefit : No more rent payments; Tax perks ; Monthly rental income; Tax deductions

Main Risk : Market value may drop; Tied to one spot , tenant issues, maintenance costs, vacancy

Typical Location Near work, schools, and family High-demand rental hubs (Commercial/Urban)

Financial Breakdown: Costs and Returns

Let’s get down to the “nitty-gritty.” Money talks, and when it comes to home property, it usually shouts. To answer the question, “Should I buy an investment property or a first home?” we have to look at the cold, hard numbers.

The Upfront Costs: Breaking the Bank

Buying property is expensive, and the entry barrier varies by path. For a first home, you are usually looking at a deposit of 20% to 30% of the purchase price. In Pakistan, the government sometimes offers schemes like the Mera Pakistan Mera Ghar (though availability fluctuates), which can help with lower down payments.

For an investment property, the bank sees you as a higher risk. Because you aren’t living there, the bank assumes you might stop paying the mortgage if times get tough. Therefore, they often demand a higher deposit—sometimes 30% to 40%. You also won’t qualify for first-time buyer tax exemptions, meaning your stamp duty and transfer fees might be significantly higher.

Ongoing Expenses: It’s More Than Just the Mortgage

Many people forget that the purchase price is just the beginning.

- Mortgage Rates: In 2026, investment loans typically carry a 1% to 2% Premium over owner-occupier loans.

- Maintenance: If your first home’s roof leaks, it’s a headache. If your investment property’s roof leaks, it’s a legal liability and a threat to your income.

- Property Management: Unless you want to take calls at 2 AM about a broken toilet, you’ll need a property manager. This usually costs 8% to 10% of your monthly rental income.

- Taxes: Rental income is taxable. However, you can often “write off” expenses like repairs and interest payments against that income—a luxury you don’t get with a first home.

Measuring the Returns

With a first home, your “return” is the equity you build over time. Every mortgage payment is like a forced savings account. In Lahore, property prices have historically grown by 8% to 12% annually in prime areas.

With an investment, you are looking for Total Return, which is: [Rental Income + Capital Growth] – [Expenses + Taxes]. If you buy a flat in a high-demand area, like DHA Phase 6, your rental income might cover your mortgage entirely. This is the “holy grail” of investing: being cash-flow positive.

Pros and Cons Comparison: A Direct Look

To help you visualise the choice, let’s compare the two paths side by side. Use this list to see which “cons” you are willing to live with and which “pros” excite you the most.

Pros of Buying a First Home

- Sense of Belonging: You are planting roots in a community.

- Customisation: You can renovate, expand, or landscape exactly how you want.

- No Landlord Stress: You never have to worry about being evicted or dealing with unfair rent increases.

- Tax Benefits: Many regions offer capital gains tax exemptions on your “Primary Place of Residence.”

Cons of Buying a First Home

- Illiquidity: Your money is “stuck” in the house. If you need cash fast, you can’t just sell a bedroom.

- Opportunity Cost: The money you spend on a home could have been invested in stocks or a business that grows faster.

- Maintenance Burden: Every repair comes out of your pocket with no tax deduction.

Pros of Buying an Investment Property

- Passive Income: You get a monthly check that helps pay your bills.

- Portfolio Diversification: You aren’t relying solely on your salary.

- Leverage: You can use the equity in one investment property to buy a second one, building wealth much faster.

- Tax Deductions: You can often deduct interest, insurance, and repairs from your taxable income.

Cons of Buying an Investment Property

- Tenant Risks: Bad tenants can damage your property or stop paying rent, leading to long legal battles.

- Vacancy Rates: If no one is living there, you are still responsible for the full mortgage payment.

- Market Sensitivity: Rental demand can drop if a major employer leaves the area or if too many new buildings are constructed nearby.

Market Trends and Timing

Timing the market is notoriously difficult, but understanding the current landscape in Pakistan is vital. As of March 2026, we are seeing a significant shift in how people live.

The Rise of Vertical Living

In cities like Lahore and Karachi, the “sprawl” is becoming unmanageable. This has led to a massive boom in luxury apartments. If you are looking for an investment, these apartments offer much higher rental yields compared to traditional houses. Tenants—especially young professionals and expats—prefer the security and amenities (such as gyms and backup generators) these buildings offer.

Interest Rate Realities

With interest rates staying high, the cost of borrowing is high. If you are buying a first home, you might want to wait for a slight dip or look for fixed-rate options. For investors, high interest rates mean you must be extra careful with your calculations. Your rental income needs to be substantial to ensure you aren’t “bleeding” cash every month.

When Should You Pull the Trigger?

- Buy a First Home Now If: You have a stable job, you plan to stay in the same city for at least 5-10 years, and you have a family that needs a consistent environment.

- Buy an Investment Property Now If: You have high “disposable” income, you already have a cheap living situation (like living with parents or a low-rent flat), and you want to prioritise long-term wealth over immediate comfort.

Risks and How to Handle Them

No investment is without risk. Whether it’s your own home or a rental unit, things can go wrong. The key is to have a plan before the crisis hits.

Risks for First-Time Homeowners

The biggest risk is “Over-leveraging.” This happens when you buy a house that is so expensive that you have no money left for anything else—often called being “house poor.”

- The Strategy: Follow the 3-5x income rule. Your total home price should ideally not exceed five times your annual household income. This gives you a “buffer” if interest rates rise or if you face a temporary job loss.

Risks for Property Investors

The biggest risks here are bad tenants and long vacancies.

- The Strategy: Never skip the vetting process. Check references, verify income, and use a professional property management service. Additionally, always keep an “emergency fund” equivalent to 3-6 months of mortgage payments. This ensures that even if the property sits empty, you won’t lose it to the bank.

The “Hybrid” Approach

Don’t forget that you can change your mind! Many people buy a first home, live in it for 5 years, and then move out and turn it into an investment property. This allows you to benefit from first-time buyer grants initially, while still building a rental portfolio later.

Decision Framework: The Ultimate Quiz

Still stuck? Take a moment to answer these questions honestly. Grab a pen and paper and tally up your “Yes” answers.

1. Do you have at least 6 months of living expenses saved in an emergency fund? 2. Are you planning to stay in your current city for more than 5 years? 3. Does the idea of fixing a leaky faucet yourself sound better than calling a property manager? 4. Is your primary goal to have a “forever home” for your family? 5. Do you have a low tolerance for financial risk and market fluctuations?

Results:

- Mostly YES: You are likely ready for a First Home. You value stability and are looking for a lifestyle upgrade.

- Mostly NO: You should consider an Investment Property. You are focused on growth, flexibility, and building a financial legacy.

FAQs Frequently Asked Questions

Should I buy an investment property or a first home first?

It depends on your current living costs. If you can live cheaply (or for free with family), buying an investment property first lets you build equity faster. If your rent is very high, buying a first home to replace that rent is usually smarter.

Which option has better tax benefits in Pakistan?

A first home often gets lower “transfer” taxes and stamp duties. However, an investment property allows you to deduct expenses like maintenance and mortgage interest from your taxable rental income.

Can I use a home loan to buy an investment property?

No, banks usually have different products for each. Investment loans generally require a higher down payment and have slightly higher interest rates because they are considered higher risk.

What is “Rentvesting”?

Rentvesting is a strategy where you rent a home to live in (usually in a place you love but can’t afford to buy) while buying an investment property in a more affordable, high-growth area.

Is a good time to buy property in Lahore?

With the urban expansion and the shift toward high-rise living, certain sectors like DHA and Gulberg remain strong. However, high interest rates mean you must ensure your “numbers” work before committing.